What Now?

I spent the past two weeks worrying aloud that I thought literally slamming the door on the US economic engine was nearsighted, silly and an idiotic move. Sadly, the economic news over the last 72 hours exceeded even my worst projections – along with those of almost every economist. Most figured the US economy would teeter at around 6 or 6.5% unemployment through April, with growth shrinking by about 10% for Q2 after zero growth in Q1. Instead, we now know that we’ve already bled almost 10 million jobs and the unemployment rate has already zoomed to 9.5 or 10%. We also know the economy contracted by about 0.8% in Q1. Along with those (now rosy) projections about how the economy was doing in March, we can also expect the similarly anticipated “V-shaped” recession is about as unattainable as the Ark of the Covenant.

I could sit here and angrily type my frustration that the government decided to shut everything down in the middle of the best economy I had experienced since I was in my mid-20s. (Trust me, I’m tempted!) But as my grandmother loved to say, “There’s no sense crying about the spilled milk. Better to get a mop and clean it up.” So how do we clean up the mess we created?

When I first started writing this yesterday, I planned on including lots of charts and tables, relying on data to drive my points home. But nothing seemed to grab my attention. Then I remembered something when I first started in sales all those decades ago. People rarely make decisions based on data. Oh, we all love to pretend we do. We convince ourselves that we are supremely rational beings. Reality is different: we are emotional creatures first and foremost. When confronted with a decision, even the most clear and concise arguments will get overwhelmed by our strongest emotions: love, hate and fear.

Especially fear.

Last week, I wrote “How many people will end up dying from COVID-19 vs. how many people will die from starvation and other diseases of poverty if the economy slips into another massive depression?” That is still the question we should be focused on. People are afraid. They’re afraid of dying. They’re afraid of their parents dying, they’re afraid of their children dying, they’re afraid of their spouses dying. But the narrative spun by both the media and the punditry is that because of COVID-19, the deaths we fear are more immediate. They’ve taken everyone’s fear of death and added the element of immediacy, and then told us the only way to eliminate the immediacy is to wall ourselves off in our homes.

This is as much a political crisis as it is a medical and economic one. As much as the media is distrusted these days (and for good reason), it’s important to note that they are getting their cues from the political class. When the governor of New York is on television daily, declaring he needs tens of thousands of non-existent ventilators or else people are going to start dying in the streets, we sit up and take notice. When the governor of Pennsylvania takes to the airwaves to declare that this is the gravest crisis we have ever faced, people heed his words. When the President of the United States begins a daily briefing by reciting the litany of the dead, we are left with the impression that our lives are about to be snuffed out.

Now, imagine if our political leaders were to go back to the original premise of “which is worse: the deaths that will result from an economic depression plus COVID-19, or just the deaths from COVID-19?” Well, then we still understand the immediate effects of COVID-19, but we’re also asked to consider the long-term effects. Why? Because unless we’re completely irrational our psyche is now forced to realize this is a life-and-death decision no matter which way we decide. People, maybe even people we love, maybe even ourselves, will die. The only question then becomes how to balance the equation so that as few people die as possible.

It’s rare that a moral question can be summed up with an equation, but this one can:

Cnm ⸫ Cm+D

Where C stands for deaths from COVID-19, D for deaths from an economic depression, and m for mediation. What is the relation between those three factors? How do we mitigate the number of deaths in each scenario, and at what point does Cm+D cross to become less than Cnm?

(Sorry. The old data guy couldn’t resist throwing mathematics into the pot.)

We know our current approach is definitely going to result in D, and we also know the human toll of D – in famine, malnutrition, abuse, and exposure – will be dreadful. Here’s what else we’re finding out: countries that shut down even further than the US and then tried to “return to normal” – like China, South Korea and Singapore – have had recurrences of COVID-19 that are even worse than their initial outbreaks. So does that combination mean we’re just screwed? We can’t restart and try to to return to normal without killing more people, and we can’t stay in our current stance without killing more people?

No. Not at all.

The key is we can reopen our businesses, pray they return to solvency and that replacements for those that disappeared come alive quickly, but with a couple of caveats.

- First, we need to understand that normal has changed. Medical science has shown that coronaviruses are, in general, highly mutable: that is, they make up for the fact they are not difficult to destroy by mutating, often quickly, meaning most treatments are not terribly effective. It’s why the “flu shot” is rarely more than 50% effective, and why nobody has yet come up with a cure for the common cold. The mediation efforts we put in place now are likely to remain with us for a long, long time.

- Second, those most at risk from COVID-19 should be isolated from the rest of the population as much as practicable. If you have bad lungs or a compromised immune system, you should stay at home as much as possible. When they fall ill and require hospitalization, they should be moved to separate wards from the remainder of the population.

- Third, the nature of white-collar work should change. I understand many jobs require you to be onsite in order to perform your tasks. Most white-collar work does not. I never understood the resistance to telecommuting; I was doing it 15 years ago and hardly ever “went to the office” for the last 6 years of my career. I think most companies are now realizing that the phobias they had about telecommuting were not well founded and having already put in place the systems that allow remote work, will stick with the model going forward.

- Fourth, the nature of school should change. Just as white-collar workers don’t need to be in a cubicle to do their job, students needn’t be tied to a desk in a building to successfully learn. Yes, there are details that would need to be worked out so far as socialization goes. Yes, it might impose a secondary hardship on families that think both parents need to work. But in an era when school districts across the country are spending billions on trying to maintain crumbling school buildings, buildings often inadequate to meet current needs, continuing with teleschool only makes sense.

Finally, our society needs to accept that some portion of the population will contract the COVID-19 disease each year. It is the nature of the virus. Every time I hear a politician, doctor or commentator talk about “defeating coronavirus,” I cringe. It’s not that eradicating the virus isn’t a worthy goal. It is, however, ridiculous to set that condition as a benchmark for returning to living.

This will probably be the hardest adaptation for our society to make. After all the hype, the shutdowns, and the panic, the idea that this is a new reality – one with yet another dangerous disease – in our midst will be difficult for many to accept. We like to think man is invincible and master of his environment. The idea that nature sometimes refuses to be tamed is a concept that we haven’t truly dealt with for nearly a century.

But if we don’t, we will have destroyed the economy that powers modern civilization. And we will have forgotten that most important of American traits: liberty. A free people do not willingly chain themselves and they are not willingly chained. It’s time we remembered that which makes us strongest and unique, and put those principles into action.

The Numbers Don’t Lie. All the President’s Men Do.

On Friday, the latest “jobs report” was released by the Bureau of Labor Statistics.Naturally, the White House jumped on the headline numbers to show how wonderful Obamanomics is working. 223,000 more jobs! Unemployment down t0 5.3%!

Except…the numbers aren’t nearly that rosy. Even long-time supporters in the financial media are taking notice that something smells as rotten at the BLS as a fish left out in the summertime Washington sun. Consider these headlines:

FiveThirtyEight: “Don’t Let The Disappointing Jobs Report Distract From the Long-Term Trend”

MarketWatch: “A ‘Soft’ June Jobs Report on Balance, Economists say”

Huffington Post: “That 5.3 percent Unemployment Number Makes the Jobs Market Look Better Than It Is”

If you’re a liberal President hoping to convince the American people about the wonderfulness of your economic program and you can’t even fool the devout Keynesians at HuffPo, it’s time to admit defeat, I would think. But I digress.

So, how has it come to this point? How have the BLS’ headline numbers become essentially meaningless? The answer is those numbers have been filtered, altered and cranked so much over the past five years that they really don’t have any meaning any more. Unlike the past, that 5.3% unemployment figure doesn’t really track the number of Americans who need a job, nor does it represent the number of jobs Americans are actually getting.

The unemployment rate and employment numbers were once based on hard data, taken from a sampling of the F1000 and 150 selected smaller companies. Since 2011, it’s based on a phone survey: literally, the BLS calls 1,000 Americans and asks them if they’re working, when they were hired and what kind of job they have, and how much they get paid. No wonder the headline employment numbers and unemployment rate is revised more often than I go food shopping. In the latest report, for instance, the BLS revised the employment numbers down by some 60,000 jobs over previous reports (more on this in a moment). Quite frankly, the government’s main jobs accountability office doesn’t really know how many people are working, where they’re working, when they get hired and when they get fired. Their data doesn’t lie, but it is actually too volatile to be a predictable indicator of what’s happening.

Second, the unemployment rate was once a solid indicator of the number of Americans who were, well, unemployed. But in 2003, the BLS changed the definition of an unemployed person from somebody who wasn’t working, but eligible to work, to somebody who was out of work and actively seeking employment. Seems like a subtle difference, but in today’s job market it’s proving to be very consequential. Additionally, BLS never counted part-time employees as “fully employed” until 2011 (funny how that date keeps coming back, more on that later, too). In the current BLS reports, all part-time employees are counted as fully employed, even if the employee would rather work full-time but can’t because their employer isn’t offering them full hours. So, that %.3% looks pretty good. It is certainly within historical norms, until you recognize that the old methodology used to get that number was much more restrictive – and accurate – than the current one.

Now, regarding that revised employment number. First, to understand what even the original number means, you have to understand that every month the US adds more people to the work force. Yes, the “Baby Boom” generation is retiring, but what you rarely hear about is that the number of “Millenials” actually outnumbers the number of “boomers.” Left-of-center economists and commentators are doing their best to make it sound as if the percentage of working age Americans is shrinking. In reality, it’s a population growing at a rate not seen since the 1960s, around 215,000 more people get added to the workforce than leave through retirement each month. In order to maintain employment levels, that means that number of jobs needs to be added to the economy each month. Fall below it, unemployment should rise. Come in above it, unemployment should fall. A 223,000 jobs gain should have kept unemployment essentially flat. Losing 60,000 jobs should have made unemployment go up. And a newly revised job gain of 664,000 for the quarter vs. working population growth of 645,000 should mean that unemployment dropped by 0.05% for the quarter. Yet, it dropped by 0.2%. Eh, what?

This comes back to the magic of not counting everyone who’s unemployed as unemployed, Today, Barack Obama’s government either calls them “marginally attached” or ignores them completely. The “marginally attached” are those that would like a job, but have simply given up hope of ever finding one. By BLS own estimate, that’s 1.9 million people. In June, the Obama administration moved over 400,000 people from unemployed to “marginally attached,” based on a phone survey yhat probably ignored them altogether. And it lends itself to another number the boys at Obama’s Labor department haven’t figured out how to fudge yet: the labor participation rate. That’s the number of Americans of working age who are, in fact, working. It’s also been dropping for the past six years, even as the unemployment number keeps dropping. If that seems like a contradiction, that’s because it is. Obviously, if the working age population is growing but the percentage of people working is dropping, unemployment should be rising. And when the LPR is at a level not seen since the Great Depression (in June, according to BLS, it stands at a 72 year low of 62.6%. The last time the LPR was this low was in the late 1970s, when unemployment reached a staggering 13.5%). it stands to reason that the unemployment number should be in the double-digits. Look, there’s a little followed, “unofficial” unemployment number called the U-6. It actually counts the “marginally attached” as unemployed. And it currently stands at…12.1%.

The idea that more than a third of working age Americans are choosing not to work is ludicrous on it’s face. But the government tells us unemployment is falling. No wonder that smell from the doors of the Labor department keeps getting stronger.

As mentioned, the changes that have allowed employment numbers to be spun so dramatically were implemented in February 2011, shortly after Barack Obama’s policies were soundly rejected in the 2010 midterm elections. I mean, that could be a coincidence. I suspect, however, there was a conversation in the Oval Office that demanded better employment numbers, that couldn’t be easily refuted by economists and could be easily embraced by Keynesians and newspapers. He got what he wanted: a way to lie, to spin, and to let his Sunday morning spokespeople lie and spin, without actually lying.

That smell coming from the Oval Office is not dissimilar from the one coming from BLS, and the President may want to check his trousers. Obama may have reached the end of this propaganda cycle. The papers have begun to notice some things that all economists, whether left or right, know to be true: full employment should yield higher wages and more hours. But hours worked fell throughout the second quarter and wages remained flat. They also know their favorite boogeyman, the evil Wall Street CEO stealing workers wages, doesn’t really fly when the stock market has also remained essentially flat. In other words, with all that extra productivity from all of those new workers, there should be a lot more money entering the economy – but there isn’t. And it isn’t ending up in the mega-bank vault, either. It just doesn’t exist.

With the biggest lie ever told by a President finally being exposed (even bigger than, “If you like your plan…), all I can do is wonder what Obama is going to throw at us next.

The Hangover

I’m pretty sure everyone reading this has experienced a bad hangover after a night of too much partying. You wake up with an oversized cotton ball in your mouth, your head is ringing like a fire bell, you have strange cravings for McDonald’s French fries and you can’t seem to move faster than a poorly fed snail. You want to kick yourself. Yeah, the party was awesome (and you still can’t find that missing lamp shade), but man, the hangover is more price than you wanted to pay.

I get the feeling many on the left are feeling something like that today. First, after the euphoria of Bill Clinton’s speech Wednesday night, they had to deal with a less than impressive performance from Barack Obama last night. Either Obama’s speechwriting team needs a shake-up or the President is out of ideas; most of what we heard last night is best summed up as “Hey, I want a do-over!” Most media outlets, including admittedly left-leaning publications like the NY Times and Politico, panned the speech as not one of his best efforts.

Then, along came this morning’s jobs report from the Bureau of Labor Statistics. No wonder the president wants a do-over.

By now, you probably read all of the doom-and-gloom reporting about it. Make no mistake, this was a pretty lousy report. But worse than the numbers themselves is what it all means when you actually dig into them a little.

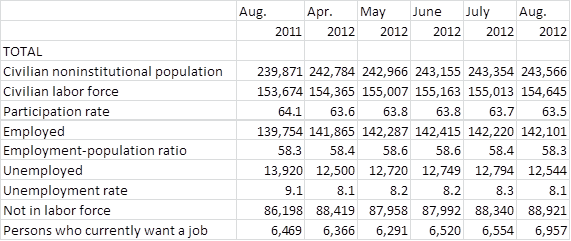

First, the headline numbers: the economy only created 96,000 new positions in August, but the unemployment rate dropped to 8.1%. This should be good news for the President, right? The unemployment rate is dropping (if somewhat unsteadily) and may actually get under the magic 8% mark most pundits think is needed if Mr. Obama is to have a real shot at reelection. And 96,000 new positions is better than no new positions, right?

Well, yes, sort of. For a better picture of why the jobs report is foreshadowing a major problem, see figure 1. This is the raw BLS data for the past year. Before your eyes begin to glaze over, there are three numbers to pay particularly close attention to.

3,965,000

1,808,000

2,723,000

The first number is the increase in the working age population over the past year. The second is the number positions created in the past year. That last one? That’s the number of working age Americans who simply gave up looking for a job in the past year. To put it another way, more of your friends, relatives and neighbors gave up the hope of even finding a job than actually found one. Nearly a million more, in fact. That’s one million American’s who are now dependent on some outside source just for survival, be it a friend, relative or the handout machine that’s become the US government.

Most economists say we need between 110,000 and 175,000 new jobs each month just to keep up with population growth. But when you look at the actual increase in working age population, the average number actually needed is around 330,000. This is very bad news for team Obama, otherwise he could point to the average of 150,000 jobs created over the past year and claim that his policies are working, albeit slowly. But the reality is that his policies are, at best, creating jobs at only half the rate needed to bring the US back to full employment.

This is particularly troubling, given that every other indicator says we should have been creating jobs at a much faster pace over the past 24 months. If you look at hourly wages, those increased by an average of 3 cents per month between March 2010 and June 2012. Although not at the level of increase seen during the Reagan, Clinton or Bush recoveries, it is still stronger than historic wage growth. Worker productivity across all sectors is also nearing an all-time high and produced solid gains during the same period. Taken together, high wage growth and productivity gains always produced significant jumps in employment before – but not now. What could possibly be holding back the “jobs engine”?

The BLS publishes an “Employee Cost Index” on a quarterly basis, and a large part of the answer can be found there. While wages and productivity show considerable growth, the ECI is also growing – in fact, it’s grown by nearly 11% since March 2010. Of that, change only 18% is represented by increased wages and a 12% drop in non-cash benefits (things like health coverage and gym memberships) counterbalances that number. So, where is the additional 10.3% in employee cost coming from? The answer is a combination of regulatory costs and taxes, the results of 3 years of this administration’s ceaseless efforts to tie nearly every industry into a Gordian knot of inefficiency. New regulations and business taxes now exceed the productivity gains made by our nation’s workforce by a 4:1 ratio, effectively wiping out the need to hire. Indeed, those costs are probably now the single biggest impediment to real employment growth our nation faces. After all, if you owned a business, you would need to be looking at explosive growth potential, not just modest growth, before bringing that much excess on board.

Many of my friends on the left insist that breakneck pace of regulations passed by the Obama administration are not having a negative effect on the economy. I submit they’re not only negatively impacting the economy, but giving business owners throughout all 57 50 states a hangover of our own.

Well, that sucked…

So, here I was winding down my little vacation and getting ready to enjoy the weekend when I opened up my email and immediately got pummeled with the headlines about the June Jobs Report. Of all the ones I saw, though, this one about sums up the employment situation best:

- Bush

- Wall Street

- Congress

- Europe

- Some combo of all the above

He’ll express some sentiment about how terrible all of this unemployment is and how, of course, he’s blameless. But hey, if I could tour closed and shuttered places of business from a tank-proof, taxpayer funded tour bus, shout out “This sucks!” to a few hundred folks and revel in the glory of being the Rock Star President – who’s to say I wouldn’t do the same?

Ok, well – back to my vaca. See you on Monday. After looking over these numbers, it looks like there’s a lot of you who’ll be able to join me for coffee without worrying you’ll be late for work. And yeah, that sucks…

Local Economics, Local Politics

When I moved my family to the NYC metro area 8 years ago, this seemed like the perfect neighborhood. Housing was relatively inexpensive, the neighborhood mix in terms of blue-collar and white-collar types, and a true representation of the American melting pot. Crime was low, the schools were better than average. In short, my town (and my neighborhood, especially) are about as representative of as you can find, with one glaring exception: this place is as solidly Democratic as anywhere in the country. The Republican party is virtually non-existent in the county and there is no local Republican organization.

I got to thinking about this yesterday after seeing one of my neighbors put a Mitt Romney sign in his yard and reflecting on recent conversations with others. There is palpable anger and despair with the current administration – anger and despair that emanates from the economic morass that Kearny, like so many other towns, finds itself stuck in. There’s a well-worn adage, coined by former House speaker Tip O’Neill, that “all politics is local.” There’s another equally well-known political saying, created by political consultant James Carville, that says “it’s the economy, stupid.” And after listening to my friends and neighbors, I found myself wondering just how exactly President Obama can win re-election. In a town where he holds an irrefutable edge in organization, he’s losing the local citizenry. And he’s losing that edge for one simple reason: the economy.

President Clueless

There’s the guy who owns the local bodega. He scrimped and saved to send his son to Columbia Law School. Despite graduating with honors and clerking at the Bronx DA’s office, his son cannot find permanent work. And thanks to the fact that nearly half of my neighbors are unemployed, his business is foundering. Where once he used to hire one or two local kids to help stock shelves, he hasn’t hired anyone. Instead, he has his cousin – an out-of-work software engineer – doing those tasks.

There’s a guy on my block who lost his job a month ago, because the company he worked for hasn’t had any new business in over a year. Despite more than 20 years working as a master stonemason, he is collecting unemployment for the first time in his life. He can’t find work. He’s falling behind on his mortgage. And he’s worried.

Around the corner, there’s a Brazilian restaurant that has cut back on their hours of operation and laid off half the staff. The woman who owns the place is in shock – three years ago she had a booming business ( you couldn’t even get a table without an hour wait) and even opened a second restaurant. Last week, she had to borrow money from her son just to turn the lights back on. She fully expects to have to shutter her business by September if conditions don’t improve.

Two doors up is a guy who owns a bakery. Every night, he leaves for work around 9pm. Last summer, he laid off his delivery driver and took to doing the deliveries himself. This summer, he’s been handing out free bread throughout the neighborhood – because orders are getting canceled at the last minute. While I’m grateful for the free bread, I wonder how much longer he can keep his ovens fired up at this pace. So does he.

After being vacant for two years, the house next door to me finally sold in May. The previous owner paid $378,000 for the property. The bank initially offered it at $290,000. The final selling price: $118,000. The new owners are excited. The rest of us looked at that selling price and weren’t quite so happy.

Down the street is an accountant I know. He got laid off in the bloodbath that was the Fall of 2009 and hasn’t found permanent employment since then. He’s surviving by taking much lower paying, no-benefit contract positions – a far cry form his former $100K salary. Where once he dreamed of sending his daughter to Princeton, the recent graduate is now headed to Hudson County Community College. And without a car – they had to sell her 17th birthday present back to the dealer, since they couldn’t make the payments.

These are just a few of the stories from my neighborhood. And as the anger seethes and despair grows, I can’t help but wonder if the President realizes he’s on a path to be remembered in the same vein as Jimmy Carter and Herbert Hoover. All because he forgot that all politics is local, and it’s the economy, stupid.

Where are the jobs?

Something to chew on over the next few days:

According to Keynesian economics, all of this government spending over the past few years should have led to an explosion of job growth. After all, since 2008 the US Government has ballooned the debt by an annualized rate of 17.47% or about twice the rate of growth over the previous decade. But the jobs aren’t coming. This first graph shows the rate of employment vs. total working age population:

Table 1: May Total Employment Ratio

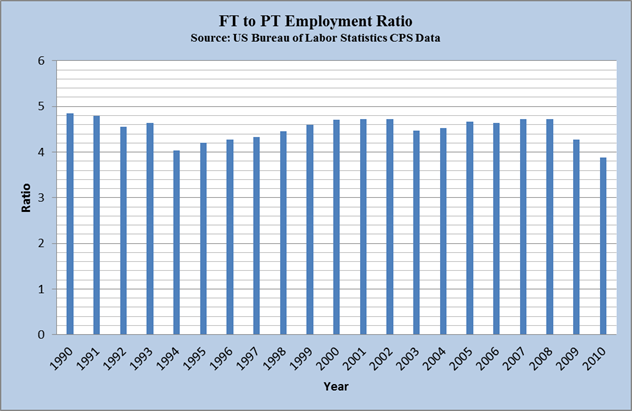

Notice that the percentage of working age people now working has dropped and kept dropping like a stone, despite all of that spending. In fact, the last time this few people had jobs was in 1982 – and prior to that, 1956, when farm payrolls were significantly higher than they are now. Now for the second half of the equation, part time employment vs. full time:

Table 2: May Employment Type Ratio

Fulltime employment has also continued to decline. Of course when you realize most of this recovery job “gains have been in retail or service industries, that shouldn’t come as a surprise. Still, the ratio now has dropped below4 FT employees per PT employee, territory we’ve never seen before. You can’t sustain a recovery on the back of McJobs. Right now, if you run the numbers, only 47% of working age Americans have a full-time job. If you’re shocked, you should be. The last time the number fell below 50% was in 1933.

If Barack Obama thinks this is the way towards recovery, he needs a new navigator.

Let the “Silly Season” begin

Once every two years, Labor Day signals the opening of the “Silly Season.” What is this “Silly Season” you ask?

Once every two years, Labor Day signals the opening of the “Silly Season.” What is this “Silly Season” you ask?

In a nutshell, the “Silly Season” is when the general populace joins political junkies in paying attention to the politicians running for office in November. And the politicians, on cue, begin campaigning in earnest. But what it makes the season silly is the way the politicians act. Suddenly, Democrats begin espousing conservative ideals. Ordinarily, they’re joined by Republicans discovering their love of liberal programs.

But this year promise to be sillier than most. With an unsettled economy, unemployment rising and public dissatisfaction in both political parties rising to all-time highs, Democrats are in serious trouble heading into the

campaign season. Many Congressional seats once considered safe for the Donkey Party are now in play; seats once considered as being in-play or toss-up’s are now leaning Republican. As reported in yesterday’s New York Times, the DNC is cutting loose many candidates, hoping to minimize losses in the November mid-terms.

In short, what many Democrats are discovering is that the positions they’ve spent the past four years carving out are not exactly what the country wanted. The reason they won most of their seats – including the Presidency – was national dissatisfaction with the Bush administration. The initiatives the current administration have pushed through have proven even more unpopular than the ones proposed by GWB. How bad is it? 56% of Americans want the abomination that passed as health care reform repealed. Republicans now lead Democrats in all ten of the major issues polls.

Not surprisingly, in light of these developments many Democrats are running as far from their own party as possible. It’s amazing how many Democrats are now against the very health care package they passed earlier this year. (Remember when Nancy Pelosi declared that once we knew what was in the bill, we would love it? Oops.) Even President Obama is finding his conservative voice, as reports suggest he will ask Congress to pass “targeted” tax breaks on Wednesday. To add to the sense of desperation from the Democrats, many are hoping to cast their opponents as extremists who would destroy the fabric of American life.

Of course, Republicans are tempted to equally join in the insanity, but so far have held the line on leaning left. They fully understand that the nation has peeked behind the Progressive curtain and been repulsed by the view. This is turning into one of the strangest elections ever seen, where the minority party is the one fending off negative attacks. Normally the reverse is true, but Republicans don’t need to go on the attack in this cycle. The news, even left-leaning organizations like MSNBC and the NY Times, can’t help but report the dismal employment numbers. So Republicans are remaining more or less silent, except to point out that the news hasn’t been good since the Obama administration took over. That’s attack ad enough. Besides, the left is self-immolating itself well enough that the Republicans don’t need to join in.

So kick back and enjoy the Road to November. It promises to be a fun – if bumpy – ride.

The Fed Announces It’s Time to Panic

It isn’t often that the political right and left in this country agree on anything, but if two articles I read this morning are any indication, we may have finally found common ground on the issue of the stagnated economy. More significantly, articles in Forbes and The Huffington Post are both sounding the same alarm bells about the Fed’s actions yesterday. If there are two publications more diametrically opposed in terms of editorial slant, I can’t think of them. After all, on most issues the Huffington Post is slightly to the left of Fidel Castro and Forbes founder (and namesake) is the epitome of neo-conservatism.

What the Fed did yesterday is press the panic button. I’m sure the President and congressional Democrats can’t be too happy about that – after all, various administration members have assiduously assured us that the economy is all fine and those of us complaining are simply making mountains out of molehills. The Fed (or more accurately, the Federal Reserve Board of Governors) said, “Um, maybe not. The economy is slowing and we’re headed for a second recession.” As their statement said,

“Information received since the Federal Open Market Committee met in June indicates that the pace of recovery in output and employment has slowed in recent months…investment in nonresidential structures continues to be weak and employers remain reluctant to add to payrolls…the pace of economic recovery is likely to be more modest in the near term than had been anticipated.”

In case your wondering, when the Fed uses terms like “slower than anticipated,” that is simply a banker’s way of saying that things are really, really bad. How bad? In the January 2010 report, the “anticipated growth rate for GDP” was 2.8% – 3.2%. If you prefer, the Fed was anticipating anemic growth already – if they’re now saying the actual rate of growth is even less than that, then it’s safe to say we’re approaching negative growth. If the economy was shedding jobs during a period of supposed growth (albeit anemic growth), what happens when growth turns negative?

Thus, the Fed is panicking. That is, nine of the ten members of the Board of Governors are panicking. (I’ll get back to the tenth in a moment). It’s perfectly understandable, since the only thing that can make a banker afraid more than a lack of government bailouts is the thought of angry mobs demanding their deposits. The actions the Fed took yesterday – converting the sizable investment in mortgage bonds they currently hold into treasuries and keeping the funds rate near 0% – indicate an organization that is under the misled belief that there isn’t enough money in the economy today.

The nine members who voted for these policies ignored a huge source of money that is available, but lacks the impetus to spend. As has been widely reported, corporations are sitting on approximately $1.8 trillion in cash assets. That equals about 12% of estimated GDP for this year – or nearly double the economic “stimulus” spent by the federal government since 2008. Those huge cash reserves, if invested back in the economy, would represent the most effective stimulus possible, since those funds would be directly spent on investment, including capital expenditures and employment. But by depressing interest rates, the Fed is holding down any incentive for businesses to invest.

This point was brought up by Thomas Hoenig, the one member of the Fed Board who didn’t vote to hit the panic button. (Told you I’d get back to him). In a nutshell, Hoenig is worried that by depressing interest rates while pumping more money into the economy, all the Fed is accomplishing is creating another bubble. Nobody is prescient enough to tell you what industry that bubble will encompass (my guess is health care), but it’s certain to come. As Hoenig pointed out, in 2003 the Fed took similar actions – and gave us the housing bubble, which led to the current recession. In 1997, the Fed took similar actions – and gave us the tech bubble.

It can be argued, and perhaps rightly, that the Fed’s overzealousness in 1997 and 2003 was warranted, since monetary policy was the best option for jump-starting stagnating economies. There is a major difference this time around, and that difference is the vast cash reserves companies have built up during this recession. The Fed’s current monetary policy is a huge disincentive for those companies to invest in what are typically long-term assets with high immediate and near-term costs; namely people and equipment. How? First, by limiting inflationary pressures, there is no reason to invest cash into something that will lose value in the near-term. Once inflation does kick in (and it will; the amount of money currently floating around plus artificially depressed interest rates guarantees it), every dollar invested now loses value not only through depreciation but also in the natural devaluation that comes with inflation. (If inflation were held at the Fed’s target rate of 5%, a dollar today would only be worth 95 cents next year). It makes much more sense, from a business perspective, to invest that money into something that almost certainly will appreciate in value. It is the mindset that explains the stock market’s insane gains this year.

So what should the Fed do? I argue the Fed should look for ways to take money out of the economy – raising interest rates and selling those securities it purchased over the past 2 1/2 years. By thus shrinking the money supply, those business currently hoarding cash are forced to begin spending again. Why? Cash flow is the lifeblood of business. Right now, business can ignore normal consumer markets because they’re making huge profits by investing their capital in the stock market, in many cases buying back their own stock and driving the prices up, ensuring positive cash flow. Once the excess cash is removed from the economy, the financial markets will react as they always do to inflation: prices will drop and indices will decline, drying up the current avenue for establishing business income. Those same inflationary pressures will force businesses to reconsider investing in long-term capital – investing their cash before its purchasing power declines.

Unfortunately, the Ben Bernanke’s and other Greenspan disciples (including the Treasury secretary) are not of a mind to engage in this type of monetary policy, fearing that jump-starting the economy by raising inflation will result in the type of over-inflation from the 1970’s and wind up uncontrollable. Oddly, many left thinking economists (notably Paul Krugman) are like-minded, although they prefer government spending over monetary policy to pump more cash into the economy. Either way, I can’t help but wonder if they’re seeing the same economic landscape those of us in the real world see. Oh, and if they realize that the policies of “priming the pump” we’ve pursued for the past 2 years haven’t worked and may very well have pushed the real economy off the cliff.

My biggest fear is they don’t see it – and they’ve taken the very social order of the first world with them in their mad dash chasing after rainbows.

Joe Fed Makes Twice What You Do (and for Doing 1/2 the Work)

More depressing news from Washington. According to this article in USA today, if you work for the federal government you’ll earn; er, make about twice as much as if you worked in the real world.

I did some back of the napkin calculations to see how much money that wastes in a year, even assuming we need all of those federal workers. (I don’t think we do, but until we get the private sector hiring again, leave ’em where they are). The number is…staggering. This is based on the average fed worker receiving $121K in annual compensation, the number specified in the article.

(Number of federal employees x $121,000) / 2=estimated overpayments

(2,150,000 x $121,000) / 2 = $130,075,000,000.

That is 130 billion, 75 million dollars.

Or, as my dear departed Granddad would say, “that’s a shitload of samoleans!” (I never really found out what a “samolean” was, but I always assumed it was something mean that traveled in big packs – like government employees).

I don’t know about you, but if the Keynesians want to spend some government dough around, I’d suggest they have a way to pay for it without adding to the debt. Simply tell all those federal employees they’re getting a 50% reduction in pay. It would also accomplish something else: all those beauracrats would actually begin to understand what it’s like to take drastic pay-cuts, only to see your job disappear 6 months later.

We can only hope…

Time for a New Consensus

One thing is becoming painfully obvious: the way we, as Americans, view economic opportunity is out of step with the way the world operates today. It is time that we recognize this and address it in a positive manner, without the political fire-bombing that is hurled daily on both the left and the right.

The left is stuck with an early 20th century Keyensian view of economics. I’d argue that particular view didn’t really work then and won’t work today. Massive infusions of government capital during the 1930’s into public works projects did build some marvelous edifices, such as the Hoover Dam, but did not absolutely nothing to end the Great Depression. America didn’t return to full employment until the advent of World War 2 – the result of increased war production and more than 10 million men entering military service. Once the war ended, the economy again returned to near-Depression era levels of unemployment. What finally proved the cure for the economic ills of the 1st half of the 20th century was that in the post-war period, only the US remained capable of providing the goods and services needed by the world. It was an export economy, fueled by international demand, which put America back to work.

The right seems permanently wed to supply-side economics. Strict adherence to that model might have worked, but we’ll never know. While government receipts during the supply-side era (1981-2008) outpaced inflation by (See fig. 1), government spending at all levels increased at an even more dramatic pace, leaving us with unsustainable levels of debt and continuing government deficits – and a seemingly insatiable public demand for services that we cannot afford.

Fig. 1

The current model being followed is a strange amalgam of the two diametrically opposed economic philosophies, with government interventions and expanded spending coupled with “targeted” tax breaks. In one sense, this new model has worked: businesses are sitting on a virtual mountain of cash. But in a much larger sense, these haven’t worked to stoke the economy – and for one simple reason, the demand needed by businesses to invest that capital doesn’t exist now. Employment data continues to remain bleak, representative of the fact that businesses are not investing in human capital. Part of the reason is undoubtedly tied to regulatory uncertainty, since anyone running a business needs to properly plan and account for the funds allocated for human resources. But that uncertainty alone cannot account for the downward pressure July’s economic data displayed on employment.

What is needed is recognition by both those on the right and the left that a new demand model is required for our current age. Modern technologies have made many labor-intensive occupations of the late 20th century redundant. Cloud computing and SaaS technology reduce the need for office and technical staffing, closing off two of the high-growth industries of the past 30 years. Manufacturing tasks that once required dozens of people can now be fully automated, with only one operator required. (Just last night I watched a documentary on Zippo lighters – the entire assembly line only needs 5 people to run it; a perfect example). Even many low-wage jobs have been replaced – the other day I went food shopping. No cashiers were available; the entire checkout line was self-service with two people running 20 checkout lanes.

In other words, there are two possibilities now facing the country:

- Current unemployment levels are now the “new normal” and a return to sub-5% unemployment is unlikely. In this event, the current social services are inadequate and need serious revamping. Unemployment insurance as currently exists needs to be discarded, replaced by a system that is more proactive in returning the unemployable to the workforce while ensuring that people are not discarded like yesterdays news. Such a program needs to be structured so that chronic unemployment and other abuses are not permitted. In short, in such a world, unemployment services should not be a state duty, they should very much be a federal-corporate symbiosis. It is impossible – and against a state’s interests – to train somebody for employment opportunities in another state, but it is in a company’s best interest to do so.

- Current unemployment levels are an aberration; a temporary result of career displacement due to a technology upheaval. Such upheavals have occurred before and the nation weathered those storms, most recently in the late-1970’s as the nation shifted from a manufacturing base to a services based economy. In this case, the government needn’t do much of anything, except make career retraining available and mandatory, in order to continue receiving unemployment insurance payments. Once, that is, the new employment needs are identified.

I’m not going to pretend I’m smart enough to know which of the two scenarios is correct. What I do know is that until we begin to honestly discuss them, no action can be planned or undertaken. But as I mentioned at the top of this post, neither side seems ready to abandon decades-old dogma. I doubt either will over the next 90 days, as we begin a new national election cycle and both sides seem to only care about scoring political points by feeding raw meat to their adherents.

It’s up to the American people to put aside our natural inclination to fear in uncertain times and force our political leaders to engage in an honest discussion of the situation. And if they won’t?

Then it’s up to us to replace them this November with people who will.

Extending Benefits

I’m certain many of you have been watching the unfolding – seemingly in slow-motion – debate on extending unemployment benefits. Then again, I’m also certain that quite a few of my fellow citizens haven’t given it more thought than which sunscreen to bring to the beach. After all, it is July. This is hardly the time of year when political juices get flowing for most of the electorate.

However, I have two strikes against me when thinking about this: for one, I am an admitted political junkie and two; I am one of those approximately 6,800,000 Americans who has been officially unemployed for longer than 6 months. (That’s a pretty dismal number, but it’s actually rosy when compared to the long-term underemployment number and the actual numbers of Americans who have been unemployed so long that the feds stopped counting them. But I digress.) So, I’ve been watching and listening with keen interest.

Being fiscally conservative (ok, ϋber-conservative) and also unable to secure new, permanent employment, I find myself torn between the two very real issues at play. Those two issues are, to put it simply, how do we reconcile a real need to prevent utter destitution for the millions like myself – and at the same time, do it in a way that doesn’t further bankrupt the country? It seems to most reasonable Americans that the proposal put forth by the Republican caucus – paying for the cost of extending unemployment benefits by using some of the remaining funds from last year’s gargantuan stimulus package – is a good compromise. Why the Democratic caucus is so opposed to the idea has been beyond me. After all, even that most liberal of economists, Paul Krugman has said repeatedly that unemployment benefits are “a highly effective form of stimulus.” Congress loves “earmarks,” or setting aside money for pet projects. In an election year when there are likely upwards of 20 million voters who face the prospect of losing everything on a daily basis, it seems logical that Congress would earmark $38 billion of pre-existing expenditures on a pretty popular program. It would be a win-win, something that almost never happens for a politician: they could claim both the labels of “caring liberal” and “fiscal conservative” with one vote. So why won’t they?

The answer (as with almost everything Congress does these days) lies in the details. The program is part of H.R. 4213, a 412 page megalith that deals with a whole of stuff not at all related to employment or economic stimulus. In fact, the section dealing with the benefit extensions is Title V, subtitle A of the bill. It incorporates all of 9 ½ pages of the bill.

I’m sure you’re asking yourself what could be in the other 402 pages of the bill. Well, here are a few highlights. Feel free to hit the link and read it for yourself:

*Provisions to build sewer systems

*Alternative fuels vehicle credits

*Energy efficient appliance tax credits

*New standards for windows and doors (You can’t make this up, folks)

*Railroad track maintenance credits

*Rum excise tax relief for Puerto Rico and the US Virgin Islands. Hey, even if we’re all broke, at least we should be able to swig cheap rum, get drunk and forget this mess!

The list goes on and on. There are over 500 individual line items in this bill. Not only have our congressmen been busy putting earmarks into this thing, it seems they’ve taken special care to pack it with more pork than a Jimmy Dean breakfast sausage. No wonder they couldn’t find the $38 billion! (By the way, by the Obama administrations own estimates, there should be nearly $340 billion left from last year’s budget buster.)

Oh, and one final note regarding the supposed disincentive of providing unemployment benefits: In ordinary times, I agree that extending unemployment benefits can be a disincentive to finding gainful employment. But these are not ordinary times; not when estimates range from five to eight people for every available job opening. And speaking from personal experience, I can assure you that getting 30% of my prior earnings in an unemployment check doesn’t exactly meet my monthly commitments. Here’s hoping Sen. Jon Kyl and Senatorial candidate Sharron Angle, who have publicly espoused this thought, take a good look around their respective states and come to their senses. They are not properly representing their constituents, their party or the nation as long as they hold that view.

Are the jobs REALLY gone?

There’s been a lot of talk lately, from both the left and the right, that most of the jobs lost in the current recession are lost forever. Robert Reich is a well-respected former Labor Secretary for President Clinton. In his article The Future of American Jobs, he contends that American jobs were permanently lost to a pair of factors: technology and outsourcing. Technology allows companies to increase employee efficiency (more employee productivity at lower labor costs); outsourcing is enabled by technology that enables foreign workers to remain competitive with Americans and can be closely monitored using new technologies. Although philosophically opposed to Reich, James Sherk of the Heritage Foundation reaches the same many of the same conclusions in Reduced Investment and Job Creation to Blame for High Unemployment. The only difference in these two articles is that Reich focuses on job losses, while Sherk focuses on job creation. But in both articles, the authors contend that both near- and long-term unemployment will remain at or near 8%. ( I wrote about the disappearing jobs phenomenon earlier this month)

There are many causes for this, of course, beginning with the fact that United States (and most of the developed world) began moving earnestly away from labor-intensive manufacturing economies towards knowledge-based service economies in the late 1970’s. Although well aware of this, nobody did much to prepare the citizenry for this fundamental economic change. Much as the US experienced a dramatic cultural and demographic shift in the late 19th century as we moved from an agrarian economy to a manufacturing economy, we are experiencing the same now. Policies over the past 30 years at both the federal and state level, rather than focusing on restructuring education and employment policies, were largely concentrated on sparing the status quo. Although the days of a high-school dropout being able to get a well-paying job for life at the local manufacturing plant ended a generation ago, we’ve continued to subsidize both the labor unions (who rely on perpetuating this myth) and the educational systems (whose labor unions and administrators have been resistant to changing the formulas they’ve worked under for 6 generations). As a result, we have a large segment of the population that is ill-suited for the type of work the modern economy provides.

Both liberals and conservatives in this country (and other Western nations) are calling for a return to 20th century economies. Liberals believe that the US can return to a manufacturing-based economy, if only certain policies are enacted. Some of these include: engaging in protectionist trade policy (apply punitive tariffs on goods produced in low-age countries); requiring a percentage of all goods sold in the US to be produced in American factories and tightening labor and banking regulations to “protect” the American worker. Conservatives are championing reduced immigration, business credits and lower taxes as the way to spur manufacturing growth. Both of these approaches – or any combination thereof – is wrong, immoral and ill-conceived. They are intended primarily to appease the 60% of Americans whose jobs will disappear or have disappeared in the past three decades.

First of all, thanks to technologies that were not even conceived a century ago, the modern world is more tightly interwoven than at any time in history. When combined with the fact that the days of imperialism ended with WWII, it is now impossible for any nation that relies on exports for economic vitality to successfully engage in protectionist trade policies. Imposing excessive tariffs or limiting imports in any way will, in the end, prove counter-productive as other nations reciprocate the move. Many persons in what we often derisively refer to as the “developing world” consider the steady income provided by manufacturing economies as a vast improvement in their situations. Despite wages that are considered substandard in the west, the mere fact that workers have a steady source of income – and therefore, food and shelter – provides a sense of security previously unknown. This was, by the way, the same attitude that drove many former tenant farmers to migrate to cities during the late 19th and early 20th centuries, in the US and Europe. This was despite the advance knowledge that most would work in conditions that we find abhorrent and for wages that we can’t countenance today. Combined with the interactive nature of modern economies, no nation can afford to block goods coming from these nations.These types of policies were tried during the heights of the Great Depression – the result was over 50 million human beings killed in the greatest conflagration in history. Secondly, imposing inane limits on immigration will rob the US of a tremendous source of energy and vigor, both of which are priceless commodities in the new economy (and I suspect that very vitality is what many are afraid of). Finally, any restructuring of tax and revenue policies that ignore the modern economic realities in favor of a long passed age robs the emerging job market of strength and future generations of Americans of a sorely needed simplified tax code.

So, if the modern economy in the West will not be based on manufacturing, what will we do in the future? Where will the jobs come from? Well, first of all, not all manufacturing will be permanently off-shored. For several reasons (including national defense), there will always be some sort of manufacturing in the US. However, the reality is that as a percentage of employment and average compensation, American manufacturing will never return to the halcyon days of the 1960’s and 70’s. The new economy will be services based and requires a more educated and more flexible workforce than the one that currently exists. I realize that when I say “services” many people conjure visions of hotel maids and McDonald’s cashiers. Those type of jobs have always existed and will always exist, but nobody should think we’ll become a nation of gas station attendants. What I’m referring to by services are the types of positions that require more brain power than brawn power; fields like medicine, technology, research, aerospace, education and banking are all services. All are creating jobs right now. The problem is, their growth is restricted by a lack of skilled workers. It’s a fact that none of your politicians want to talk about, because they know in large part they’re directly responsible for this fact.

The answers about what to do for the next generation of Americans is pretty obvious and I applaud President Obama for starting education initiatives that may prove fruitful. (I’m no fan of the President, but you have to give credit where it’s due). However, there are 2 generations of Americans now in the workforce and a third about to enter, whose citizens are ill-prepared for the current economy. The big question is what do we do about restoring some semblance of full employment, and at tolerable wages now? The first thing is for the labor unions to understand that the world has changed and they need to get with the times. Once, the antagonistic approach between organized labor and business in the US led to a system that worked well, in the contained system that was the US. Once the US was no longer the dominant player in manufacturing, though, the unions failed to keep up with pace of global economics. It is long past time for them to seriously engage foreign governments and labor markets -by working to raise living standards oversees, they can reinforce those standards back home. Secondly, our own politicians need to work in ways that remove the yoke of debt from our collective shoulders. The projected national debt for 2020 equates to $150,000 for every family in the US – or more than 3x the anticipated per family income for that year. That level of debt is unsustainable and is largely driven by “entitlement” spending – Social Security and the new Health Care package. It is past time to revisit how these programs are funded before they drive the entire nation into bankruptcy. Until debt projections are reduced, funding for projects needed to revitalize the economy cannot be pursued. In the same vein, the political class needs to be honest about the limits of government intervention in economic policy – aside from fiscal and tax policy, there really isn’t anything they can do for immediate and sustainable growth. At the moment, fiscal policy is stagnated -interest rates are at zero. That leaves tax policy – which will not unfreeze capital markets. However, by implementing a strategic tax policy in coordination with a debt reduction plan, lawmakers can relax market tensions by demonstrating long-term fiscal sense.

However, even if the various entrenched factions were to begin immediately putting these ideas in action, the near-term effect would be negligible. We would still need high spending on unemployment compensation and other safety net program to prevent our society from devolving into absolute chaos. I would like to add a caveat to this spending, though. One thing obvious to anyone who’s driven any road in Pennsylvania or watched a manhole explode in New York City knows our infrastructure is aging badly. I would offer those receiving government assistance the option of either attending training in a new field or showing up for manual labor repairing our bridges, schools and the like. This recreation of the WPA would at least prevent the nation from just throwing money down a rat-hole.